16 December 2024

Orcadian Energy plc

(“Orcadian” or the “Company”)

Results for the year ended 30 June 2024

Orcadian Energy (AIM:ORCA), the low-emissions North Sea oil and gas development company, is pleased to announce its audited results for the twelve months ended 30 June 2024.

Highlights:

- Completed the sale of an 81.25% interest in Licence P2244 to Ping Petroleum UK plc (“Ping”), leaving Orcadian with an 18.75% interest in the Pilot Licence carried to first oil, gross reserves in Pilot are 78.8 MMbbl.

- Awarded three new licences in the 33rd Round:

- Licence P2634, in which Orcadian has a 50% interest, contains a large viscous oil discovery, Fynn Beauly, which could provide a suitable feedstock for anode grade cokers, which can create the synthetic graphite used for EV anodes. Serica has recently announced the intended acquisition of Parkmead (E&P) Ltd, the operator of this licence. The Company are delighted to welcome Serica on to the licence and look forward to progressing this project with Serica as operator.

- Licence P2650, in which Orcadian has a 50% interest and is operator. This licence contains shallow gas prospects which can be drilled at low cost. Prospective resources are some 269 bcf of gas.

- Licence P2680, in which Orcadian held 100% at 30 June 2024, that contains the Earlham discovery (114 bcf, contingent) and the Orwell redevelopment project (31 bcf, contingent), as well as the Clover gas prospect (153 bcf, prospective).

- Since the end of the period under review:

- Agreement to sell a 50% interest in a sub-area of Licence P2680, containing the Earlham and Orwell fields, to The Marine Low Carbon Power Ltd (“MLCP”) leaving Orcadian with a 50% interest in the sub-area of the Licence carried to first gas. Gross recoverable fuel gas contingent resources in Earlham and Orwell are 145 bcf;

- Shell loan assigned to The Independent Power Corporation Ltd (“IPC”) and agreement to settle the loan as part of the proceeds from the sale of the P2680 licence interest to MLCP;

- Acquisition of HALO Offshore UK Ltd (“HALO”) and subsequent sale of a 50% interest in HALO to IPC, with IPC providing access to acquisition finance; and

- New focus on acquiring producing licence interests on the UKCS through HALO which has incurred £52.6 million of pre-trading capital expenditures which should provide allowances to offset against tax payable on any producing licence interests to be acquired.

The full financial statements are available at this link:

https://orcadian.energy/wp-content/uploads/2024/12/FY24-Financial-Statements-FINAL-fully-signed.pdf

Steve Brown, Orcadian’s CEO, said:

“2024 has been a very busy period for the Company. We completed on the sale of Pilot and are working with the operator to progress the project once regulatory and fiscal clarity emerge in the Spring.

We also accepted all the licences that we applied for in the 33rd round and had always seen Earlham as a project that we could move rapidly towards development. Partnering with MLCP, who have been working on the design of an offshore power station with integrated carbon capture for four years, made great sense to us. We are delighted to be supporting MLCP in the delivery of this project.

Finally, we acquired HALO Offshore UK Ltd and will bring IPC in as an equal partner to enable HALO to acquire producing assets on the UKCS with an objective of turning HALO into a dividend paying entity as soon as possible.

We look forward to the year ahead and progressing all these projects with our partners.”

Report and Accounts and Annual General Meeting

A copy of the annual report and accounts for the year ended 30 June 2024 will be available on the Company’s website (https://orcadian.energy) with effect from today. The Company will be posting its annual report and accounts and notice of Annual General Meeting (“AGM”) to its shareholders on 19 December 2024.

The AGM will be held at the offices of Shakespeare Martineau, 60 Gracechurch Street, London, EC3V 0HR at 10:30am on 15 January 2025.

For further information on the Company please visit the Company’s website: https://orcadian.energy

Contact:

|

Orcadian Energy plc |

+ 44 20 7920 3150 |

|

Steve Brown, CEO Alan Hume, CFO |

|

|

Zeus (Nomad and Joint Broker) |

+44 20 3829 5000 |

|

Dan Bate / Alex Campbell-Harris (Investment Banking) Simon Johnson (Corporate Broking) |

|

|

Novum (Joint Broker) |

+44 207 399 9425 |

|

Colin Rowbury / Jon Belliss |

|

|

Tavistock (PR) |

+ 44 20 7920 3150 |

|

Nick Elwes / Simon Hudson |

Qualified Person’s Statement

Pursuant to the requirements of the AIM Rules and in particular, the AIM Note for Mining and Oil and Gas Companies, Maurice Bamford has reviewed and approved the technical information and resource reporting contained in this announcement.

Maurice has more than 35 years’ experience in the oil & gas industry and 3 years in academia. He holds a BSc in Geology from Queens University Belfast and a PhD in Geology from the National University of Ireland. Maurice is a Fellow of the Geological Society, London, and a member of the Geoscience Energy Society of Great Britain. He is Exploration and Geoscience Manager at Orcadian Energy.

About Orcadian Energy

Orcadian is a North Sea focused, low emissions, oil and gas exploration and development company. Orcadian may be a small operator, but it is also nimble, and the Directors believe it has grasped opportunities that have eluded some of the much bigger companies. As we strike a balance between Net Zero and a sustainable energy supply, Orcadian intends to play its part to minimise the cost of Net Zero and to deliver reliable energy to the UK.

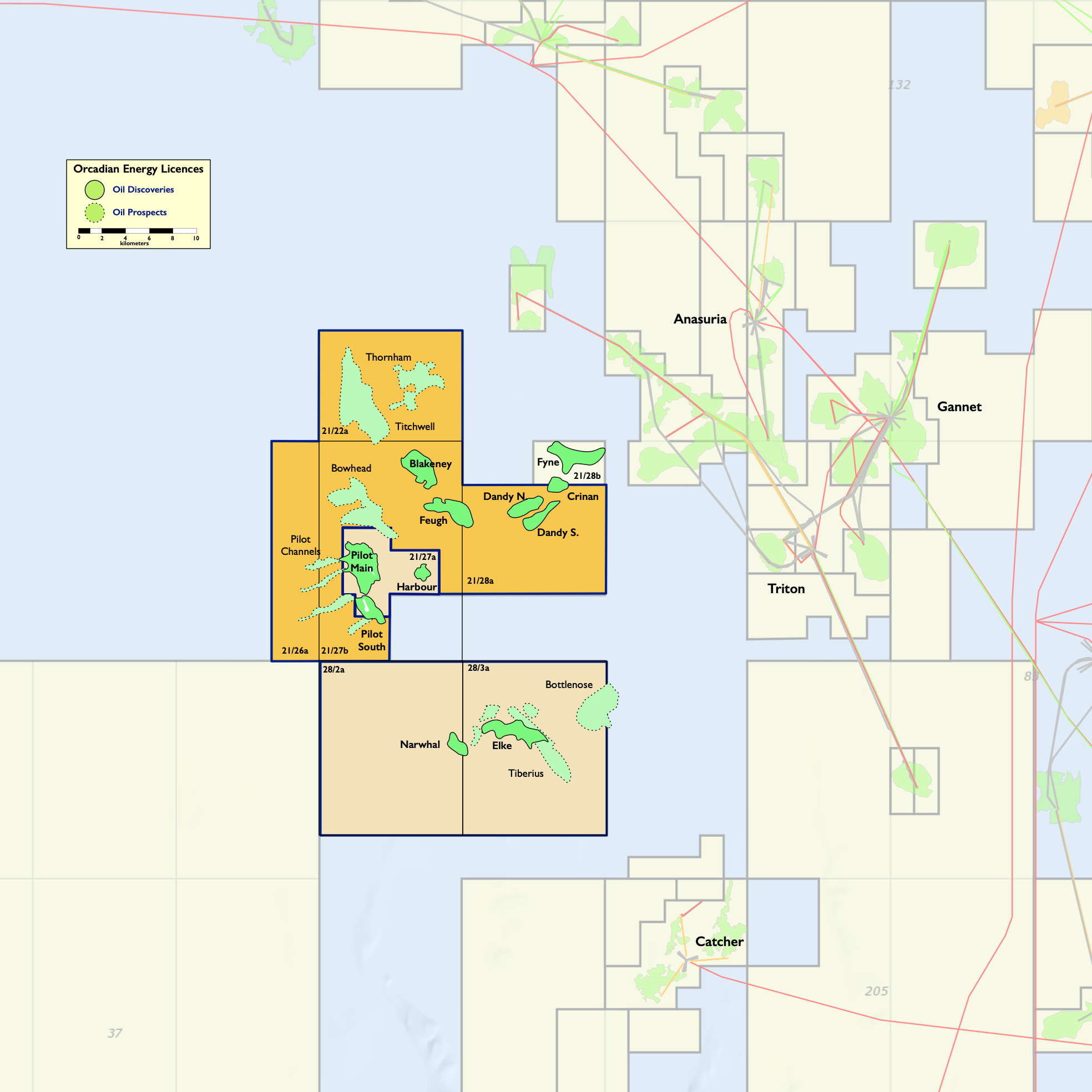

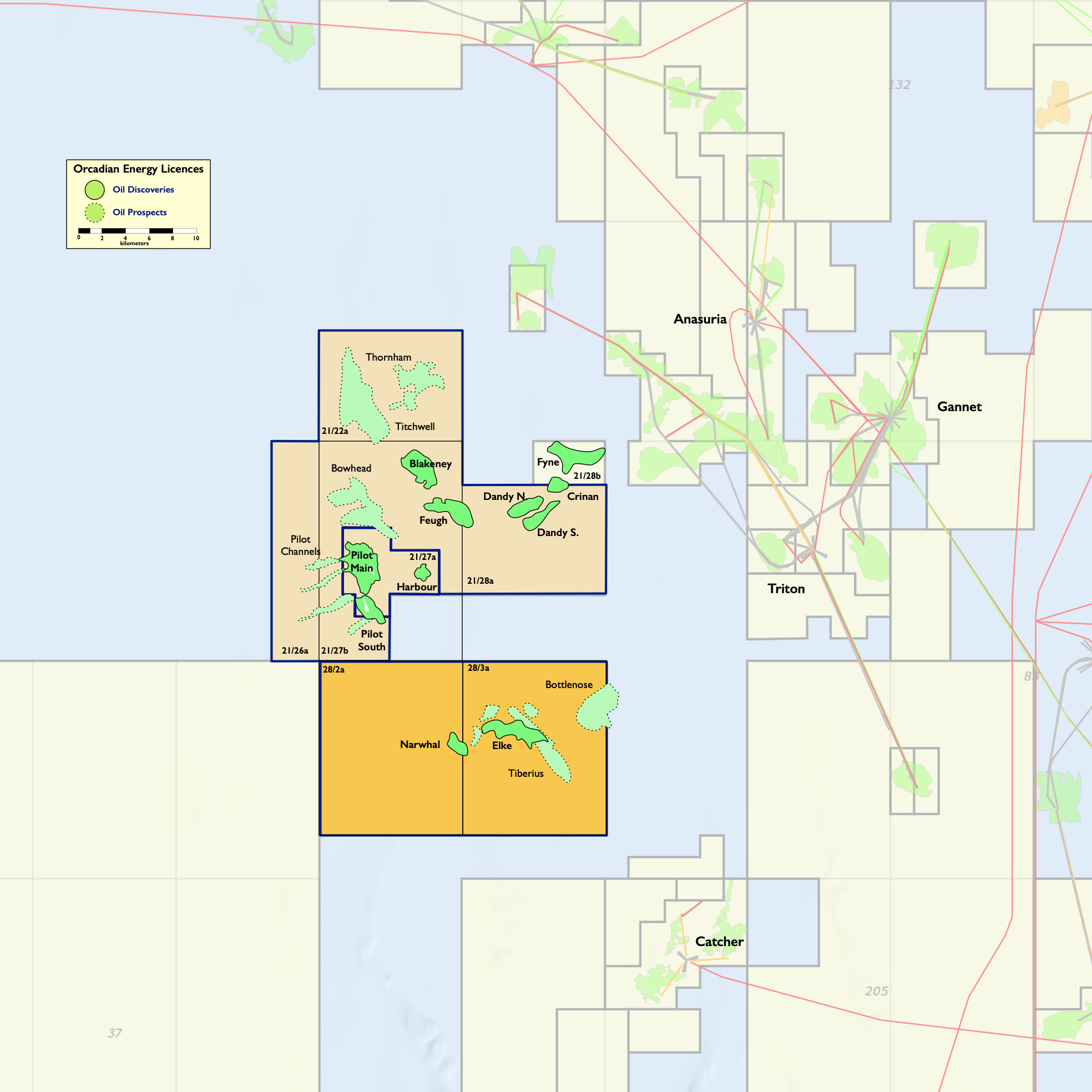

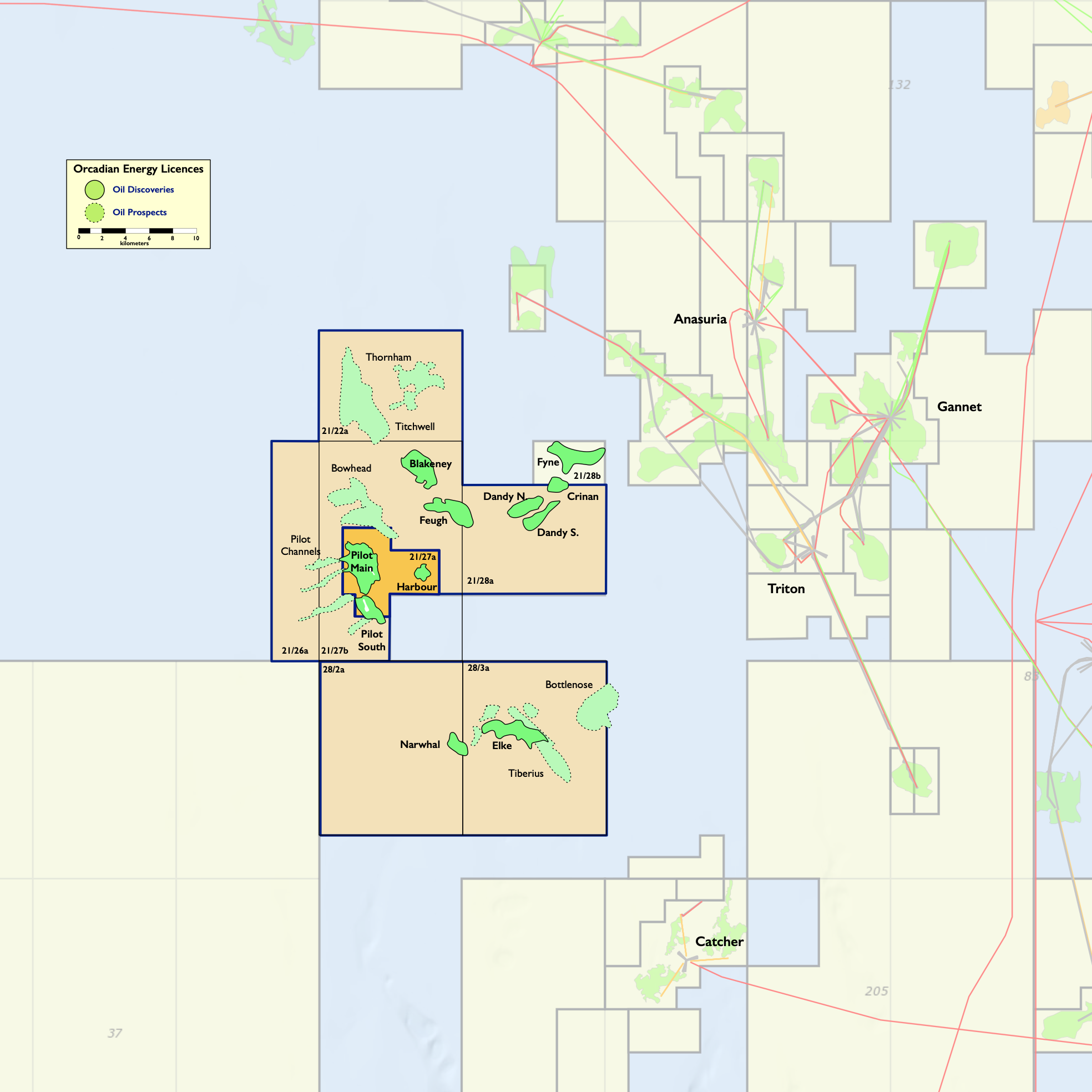

Orcadian’s key asset is the Pilot oilfield, Pilot was discovered by PetroFina in 1989 and has been well appraised. The field has excellent quality reservoir and contains 263MMbbl of a viscous oil ranging in gravity from 17º API in the South of the reservoir to 12º API in the North. In planning the Pilot development, Orcadian has selected polymer flooding and wind power to transform the production of viscous oil into a cleaner and greener process. Polymer significantly reduces fluid handling requirements and hence energy consumption as well as boosting recovery. Ithaca Energy, operator of the Captain field in the Inner Moray Firth, has enjoyed consistent success in applying polymer flood to the highly analogous Captain field. Following the recent farm-down of Pilot, the project is now under the stewardship of Ping Petroleum UK PLC (“Ping”) and is intended to be amongst the lowest carbon emitting oil production facilities in the world.

Ping is progressing a low-emissions, phased, field development plan for Pilot based upon a polymer flood of the reservoir, a Floating Production Storage and Offloading vessel (FPSO) and provision of power from a floating wind turbine or a local wind farm.

Orcadian has an 18.75% fully carried interest in licence P2244 (block 21/27a) and a 100% interest in licence P2482 (blocks 28/2a and 28/3a). Ping is operator of P2244 and the Pilot development project.

Orcadian was awarded three licences in the 33rd round. The Mid-North Sea High licence, P2650, contains shallow gas leads. Orcadian applied in partnership with Triangle Energy, an Australian listed energy company. Orcadian is licence administrator and holds 50% of the offered licence. The Mid-North Sea High licence covers blocks 29/16, 29/17, 29/18, 29/19, 29/21, 29/22, 29/23, 29/27 and 29/28.

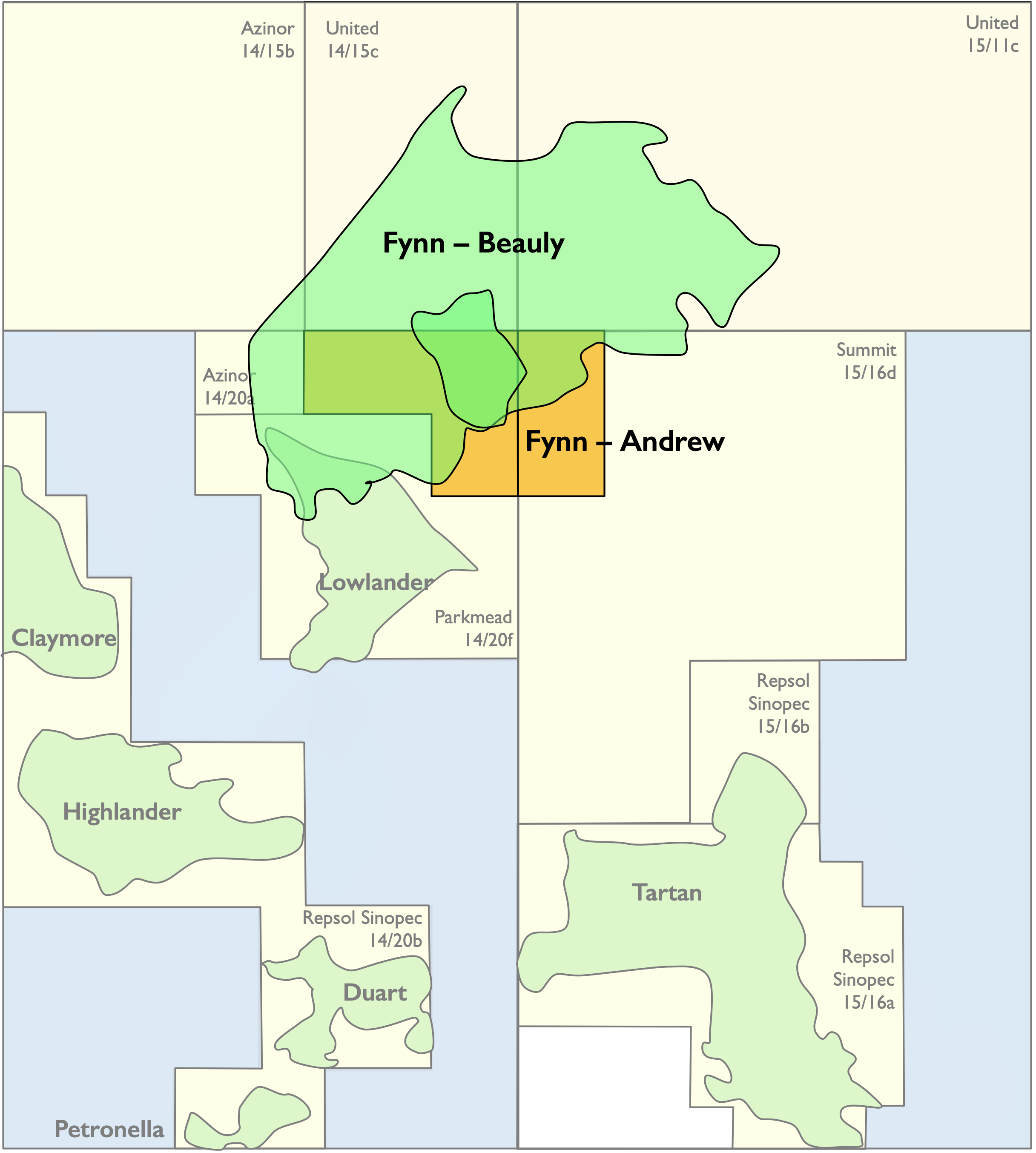

The Fynn licence, P2634, contains a very substantial heavy oil discovery. About 88% of the resource on a best technical case is estimated to lie within the area of the offered licence. Orcadian has a 50% working interest in the Fynn licence which is operated by the Parkmead Group. The Fynn licence covers blocks 14/15a, 14/20d and 15/11a.

The SNS licence, P2680, 50% Orcadian on completion of a proposed transaction, contains the Earlham discovery, a low-calorie gas discovery with 114bcf of methane resources on a P50 basis, the Clover prospect which has P50 prospective resources of 153bcf, and the decommissioned Orwell field which has redevelopment potential, alongside a number of smaller prospects. The Marine Low Carbon Power Company Ltd, an affiliate of IPC is intended to own the other 50% of P2680 and will carry Orcadian to first gas.

Chairman and CEO’s Statement

The year to 30 June 2024 has been an important period in the development of Orcadian. We closed on the farm-out of an interest in our Pilot discovery on the 31 March 2024 and welcomed Ping Petroleum UK plc (“Ping”) on board as operator of the Pilot field. We retain a carried 18.75% interest in the field, and we look forward to Ping progressing the development project once the government’s consultation on environmental impact statements is complete and the process for development project approval becomes clear and probably most important of all, the government consultation on the successor fiscal regime post-EPL in 2030 clarifies the future fiscal framework.

In the meantime, Ping is focussed on the sub-surface aspects on the development which provides the foundation of any field development plan. We are delighted to have Ping on board and look forward to both fiscal and environmental policy clarity so that the project can proceed.

In February 2024 we were awarded two Central North Sea licences and in May 2024 the NSTA announced a third tranche of licences which resulted in the award of our first Southern North Sea licence. These awards were the direct result of us following our strategy.

Our strategy stands on three legs.

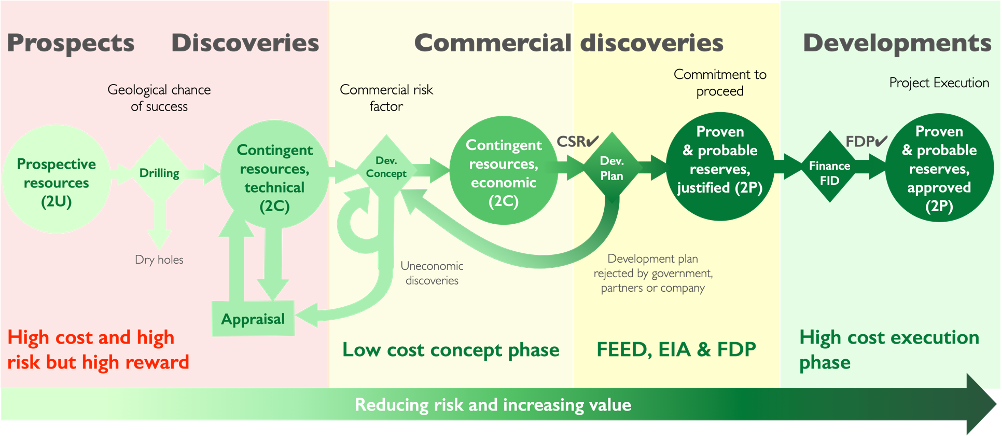

Firstly we focus on discovered and appraised fields which lack a development plan. Below is a representation of the process oil companies follow to progress leads into prospects, prospects into exploration wells, and discoveries into development projects. This process often takes unexpected turns so that projects get recycled or even discarded. We love those discards. We can make something of them, and indeed our success in farming out the Pilot project proves the model works.

So, we build the portfolio by licensing discoveries. We prefer a fully appraised field, that calls for innovation, to a great exploration prospect, but we don’t ignore great prospects. We will aim to farm out any exploration wells in our work programmes as exploring with equity rather than cash flow is folly.

So, we build the portfolio by licensing discoveries. We prefer a fully appraised field, that calls for innovation, to a great exploration prospect, but we don’t ignore great prospects. We will aim to farm out any exploration wells in our work programmes as exploring with equity rather than cash flow is folly.

Secondly, we always look for high quality reservoir rocks and aim to innovate around tricky fluids. We have a big focus on viscous oils and have built up considerable expertise in polymer flooding which can enable high recovery factors and low emissions per barrel of oil produced.

We are also content that we can handle high inerts and low-pressure gas. A big part of that is down to our development strategy for such discoveries. In short, we aim to bring the power station to the field rather than take the gas to the power station. That allows us to handle quite high levels of inert gases without significant or expensive treatment systems. For low pressure gas, as shallow gas almost always is, we don’t have to compress the gas to such a high pressure which saves energy and emissions.

Our deal with the Marine Low Carbon Power Company Ltd (“MLCP”) documented in a heads of agreement, announced on 12 December 2024, provides a clear pathway to development for the Earlham discovery. We are delighted to be working with MLCP to develop Earlham and Orwell and to have a second project where we are carried to first production. The Earlham field will be developed with a couple of horizontal wells and a downdip carbon dioxide injector. Orwell is likely a single subsea well tied back to the Earlham WHP. The Earlham WHP will be bridge linked to a Mobile Offshore Generating Unit (“MOGU”) which will generate up to 300MW of low-carbon power. Carbon dioxide separated from the well fluids and captured from the generator exhausts will be re-injected down-dip from Earlham. All of the above development planning is subject to discussions with NSTA.

Finally, we focus on what we call the post-transition hydrocarbons: gas and heavy oils with the potential to create more than just combustion products. The Fynn discovery that we share with Parkmead epitomises a post-transition hydrocarbon.

In 1977 BP concluded that in a sample of Fynn oil “the atmospheric residue > 371ºC accounted for some 88.5% wt. of the crude, but was too aromatic to be of much commercial use”. Roll forward to 2022 and Digital Refining in the Q4 magazine stated that “a highly aromatic feedstock must be used to produce premium-quality, readily graphitisable needle coke”. So Fynn could be a great feedstock to make needle coke.

But of what use is this needle coke? It turns out that one of the “recent uses [of needle coke] include the production of synthetic graphite for lithium-ion battery anode material in electric vehicles EVs.” So, production from Fynn will not inevitably be combusted as Lord Leggatt asserted in the Finch judgement. We estimate about 20% by mass will end up in the anodes of electric car batteries.

So the awards in the 33rd round were completely consistent with our strategy and we have been delighted with the progress we have been able to make in farming out an interest in the Earlham discovery.

We have agreed to sell a 50% interest in a sub-area of Licence P2680 to The Marine Low Carbon Power Company Ltd (“MLCP”). MLCP plan to develop Earlham and Orwell to supply the first of MLCP’s Mobile Offshore Generating Units (“MOGU”), which will in turn supply carbon free energy to MLCP customers and to IPC New World Energy Ltd’s (“IPCNWE”) battery projects.

MLCP is a joint venture company owned by IPCNWE and Richmond Offshore Energy Ltd. IPCNWE is part of the Independent Power Corporation PLC (“IPC”) group and is the largest developer of consented battery projects in the UK with 5.5 GW of capacity under development. MLCP has designed, in conjunction with GE Vernova and Capsol Technologies of Norway, a 300 MW offshore power facility with integrated carbon dioxide capture and distributed carbon dioxide storage offshore in a reservoir, most likely within the Licence P2680 sub-area.

Shell Loan

As part of the overall arrangements IPC has acquired the loan advanced by Shell International Trading and Shipping Company Limited (“Shell”) to Orcadian Energy (CNS) Ltd in August 2019. The amount owed to IPC and IPCNWE is US $1.5 million. IPCNWE has agreed to convert US $1.4 million of this into funding part of the consideration for MLCP to acquire its 50 per cent stake in Earlham and Orwell. The balance of US $100,000 will be exchanged for an Orcadian loan note, dated 30 June 2026, and convertible into approximately 312,500 Ordinary shares in Orcadian at a conversion price of 25 pence per share, Orcadian may require conversion of the loan note into Ordinary shares if Orcadian’s volume weighted average share price (“VWAP”) in each of five consecutive trading days is 35p or above.

Farm-out Terms

Orcadian has agreed the key terms of a farm-out agreement for a sub-area of Licence P2680 with MLCP. The principal terms of the agreements have been documented in a non-binding Heads of Agreement which defines the entire suite of agreements that need to be finalised.

It is intended that the farm-out will be implemented as follows:

- MLCP will acquire from Orcadian a 50% interest in the Earlham discovery and Orwell field redevelopment by acquiring a 50% interest in a sub-area of Licence P2680, comprising blocks 50/26 and 49/30b.

- Orcadian will act as Licence Administrator through the Assessment Phase and MLCP will become Licence Administrator for the Authorisation phase which includes the preparation and submission of the Field Development Plan (“FDP”) and the Environmental Statement.

- It is intended, subject to approval from the North Sea Transition Authority (“NSTA approval”), that on FDP approval MLCP will become Licence Operator for the project execution and operating phases of the project.

- This transaction is subject to NSTA approval and will be documented in a fully termed Sale and Purchase Agreement and a Joint Operating Agreement;

- The purchase price of 50% of the sub-area of Licence P2680 has been agreed to be US $2.2m, with US $1.4m payable on completion and two tranches of US $400,000 payable on achieving fuel gas quality production rates in excess of 50 MMscf/day for a 48 hour period, both 30 days after first gas and 120 days after first gas.

- Together with the convertible loan arrangements noted above, the payment upon completion will offset in full the amounts owed by Orcadian to IPC and IPCNWE;

- MLCP will carry Orcadian’s share of expenditure through to first gas on the development of Earlham and Orwell;

- The carry will be repayable through MLCP having an enhanced revenue interest of 80% until the carry is fully repaid.

As a consequence of these arrangements, Orcadian will retain a 50% carried interest in the development of Earlham and the redevelopment of Orwell, and its debts to Shell and IPCNWE will be paid in full.

This is a provisional agreement and there can be no guarantee that the transactions will all complete. Any deal is subject to, amongst other matters, completion of due diligence, negotiation of detailed documentation, and various regulatory consents as well as the Board approvals of MLCP and Orcadian.

Financial Results

The Group incurred a loss for the year to 30 June 2024 of £938,471 (30 June 2023 – loss of £1,184,954).

The loss mainly arose from salaries, consulting and professional fees along with general administration expenses, the impairment of intangible assets and new business development.

Cash used in operations totalled £489,787 (30 June 2023 – £599,759). As at 30 June 2024, the Group had a cash balance of £214,977 (30 June 2023 – £109,705). At the date of this announcement, the Group’s cash balance was £75,919.30.

Oil Price Outlook

Given the results of the US Presidential election and President Trump’s commitment to lower energy prices, we can expect that geology, not politics, will be the constraint on US production which underpins the world’s ability to supply energy. Predicting oil and gas prices is futile, they will either go up or down and most likely will go up and down. However, we can be confident that the International Energy Agency (“IEA”) will be surprised by the strength of demand and OPEC will be surprised by the strength of supply, averaging these two organisations projections is not a bad way to divine the future.

UK Oil and Gas Sector

The UKCS oil and gas sector has had a Field Development Plan (“FDP”) approved since the Victory gas field in January 2024 and the Rosebank oil field in September 2023. The tally of a solitary field development plan approval in 2024 seems unlikely to be surpassed by the end of 2024. The year 2021, blighted by COVID, had the same score, but we have to go back to the dawn of the North Sea in 1975, when the Forties development was approved, to find another occurrence of such a low number of FDP approvals.

The reason is clear – the government has enacted punitive taxes which limit returns and the regulatory framework has been subjected to an incessant stream of lawfare which culminated in the Finch ruling requiring every Environmental Impact Assessment (“EIA”) to take into account Scope 3 emissions.

From Orcadian’s perspective, the Finch ruling does not raise concerns for us. Quantifying the impact of Scope 3 emissions is a reasonable step, as their effect is expected to be negligible. As an example, the Rosebank field will produce about 300 MMbbl of oil, that when combusted will produce about 134 million tonnes of carbon dioxide, which will increase the carbon dioxide concentration in the atmosphere by just under 0.02 parts per million, assuming nature absorbs nothing – a very unlikely assumption given about half of the carbon dioxide emitted from fossil fuels since the industrial revolution has been so absorbed. Using the IPCC central estimate for the impact on global temperatures of a doubling of the atmospheric carbon dioxide concentration – 3ºC – that increase in carbon dioxide concentration could increase global temperature by less than two ten thousandths of a degree, far below the level that any creature could perceive.

This is why action on climate change needs global agreement on actions to reduce demand for fossil fuel energy. Constraining supply can only impact demand by increasing the price of energy; increasing the price of energy will undermine support for any climate action. So, politicians and engineers alike need to focus on delivering low-carbon energy for the lowest cost possible. That is why our Earlham project is so important. It will deliver low to no carbon energy at an affordable cost and on a dispatchable basis. We hope to learn from that project so that we can implement repeat projects at lower costs.

Nevertheless, because of the Finch ruling both Shell’s Jackdaw project and Equinor’s Rosebank project will have to be re-approved, and the government will have to re-issue guidance on how EIA documents are prepared.

The industry awaits that guidance which is expected in the Spring. However, the industry is also awaiting guidance on the successor fiscal regime from 2030 onwards. From FDP approval to first oil is typically at least three years, the earliest we might see a new project FDP approved is late 2025 or 2026. What that means is that by far the bulk of the revenue from any new project of substance will be taxed under the successor regime. So, operators’ hands are tied, they need regulatory clarity, and they need fiscal clarity.

From Orcadian’s perspective, the Finch ruling is not a cause for concern. There is no harm in quantifying the impact of Scope 3 emissions, as their effect is expected to be negligible. As to emissions in the production process we are confident that the right approach is to minimise those and to eliminate the bulk of the transportation emissions by producing oil and gas in our own backyard.

However, we will have to wait and see how government intends to tax the industry in the longer term, and we hope for a balance between ensuring a fair return for investors and maximising government revenues. It is probably true to say that the current fiscal regime is demonstrating exactly how the Laffer curve works in practice, we are on the wrong side of the Laffer curve, and in fact government revenues will rise with a more attractive fiscal regime. We are confident that sense will prevail, and the industry will have a bright future in the UK. But we will all have to wait for the outcome of these consultations before any company commits to a new development project of scale and we are optimistic that Ping will move forward with its North Sea development portfolio once the mists have cleared in Spring.

However, despite all the gloom we see great opportunity in the UK. The pendulum always swings too far and this time taxes have gone too high, and the hurdles development projects have to clear have become too many. Things will change and there is hope that the companies that stick by the UK will eventually prosper.

Business Outlook

Our near-term objectives are to complete the Earlham farm-out, and to secure producing acquisition opportunities for HALO Offshore UK ltd (“HALO”), the company we will jointly own with IPC.

Shareholders may have been surprised by this acquisition, but it has an interesting fiscal history and we and our partners at IPC see great opportunities to acquire producing licence interests which is why IPC is funding HALO to pursue such opportunities. There are a good number of companies looking to downsize or exit their UK portfolios, and not so many in a position to acquire fields. We look forward to updating shareholders again in due course.

Joseph Darby, Chairman, and Stephen Brown, CEO

13 December 2024

INDEPENDENT AUDITOR’S REPORT TO THE DIRECTOR’S OF ORCADIAN ENERGY PLC

Opinion

We have audited the financial statements of Orcadian Energy plc (the ‘parent company’) and its subsidiaries (the ‘group’) for the year ended 30 June 2024 which comprise the Consolidated Statement of Comprehensive Income, the Consolidated and Parent Company Statements of Financial Position, the Consolidated and Parent Company Statements of Changes in Equity, the Consolidated and Parent Company Statements of Cash flows and notes to the financial statements, including significant accounting policies. The financial reporting framework that has been applied in their preparation is applicable law and UK-adopted international accounting standards and as regards the parent company financial statements, as applied in accordance with the provisions of the Companies Act 2006.

In our opinion:

- the financial statements give a true and fair view of the state of the group’s and of the parent company’s affairs as at 30 June 2024 and of the group’s loss for the year then ended;

- the group financial statements have been properly prepared in accordance with UK-adopted international accounting standards;

- the parent company financial statements have been properly prepared in accordance with UK-adopted international accounting standards and as applied in accordance with the provisions of the Companies Act 2006; and

- the financial statements have been prepared in accordance with the requirements of the Companies Act 2006.

Basis for opinion

We conducted our audit in accordance with International Standards on Auditing (UK) (ISAs (UK)) and applicable law. Our responsibilities under those standards are further described in the Auditor’s responsibilities for the audit of the financial statements section of our report. We are independent of the company in accordance with the ethical requirements that are relevant to our audit of the financial statements in the UK, including the FRC’s Ethical Standard as applied to listed entities, and we have fulfilled our other ethical responsibilities in accordance with these requirements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our opinion.

Material uncertainty related to going concern

We draw attention to note 2.3 in the financial statements, which indicates that the group and company are reliant on raising finance within the 12 months following the date of approval of these financial statements in order to meet its working capital requirements and continue to fund further exploration expenditure over this period. As stated in note 2.3, these events or conditions, along with the other matters as set forth that note, indicate that a material uncertainty exists that may cast significant doubt on the Group and Parent company’s ability to continue as a going concern. Our opinion is not modified in respect of this matter.

In auditing the financial statements, we have concluded that the director’s use of the going concern basis of accounting in the preparation of the financial statements is appropriate. Our evaluation of the directors’ assessment of the Group and Company’s ability to continue to adopt the going concern basis of accounting included:

- Reviewing the accuracy of historical forecasts by comparison to the actual results in the year to assess the accuracy of management’s forecasting process;

- Assessing and challenging the key inputs and assumptions in the underlying cashflow forecasts prepared by management covering the going concern period; and

- Discussing strategies regarding future availability of funding and assessing the likelihood of the required funds being successfully raised by considering the funds required and the Group’s and Company’s ability to raise such funds. This has included obtaining and reviewing key terms of various agreements entered into after the year end.

Our responsibilities and the responsibilities of the directors with respect to going concern are described in the relevant sections of this report.

Our application of materiality

The scope of our audit was influenced by our application of materiality. The quantitative and qualitative thresholds for materiality determine the scope of our audit and the nature, timing and extent of our audit procedures. We also determine a level of performance materiality which we use to assess the extent of testing needed to reduce to an appropriately low level the probability that the aggregate of uncorrected and undetected misstatements exceeds materiality for the financial statements as a whole. In determining our overall audit strategy, we assessed the level of uncorrected misstatements that would be material for the financial statements as a whole.

Materiality for the consolidated financial statements was set as £79,000 (2023: £80,000) based upon net liabilities (2023: gross assets). There has been a change in the benchmark in the current year in comparison to the prior year. Given the stage of development of the group, at present the capitalised exploration costs and borrowings of the group are considered to be the area of most interest to users of the financial statements. Performance materiality and the triviality threshold for the consolidated financial statements were set at £55,300 (2023: £56,000) and £3,950 (2023: £4,000), respectively, a level considered appropriate given our accumulated knowledge in respect of the group and the assessed level of risk.

Materiality for the parent company was set as £78,000 (2023: £79,000) based upon gross assets

(2023: gross assets). Gross assets were considered to be an appropriate basis due to the fact that the most significant balance within the parent company is the investment in the subsidiary, and the assets within this subsidiary will determine the future success of the group. Performance materiality and the triviality threshold for the company were set at £54,600 (2023: £55,300) and £3,900 (2023: £3,950), respectively, a level considered appropriate given our accumulated knowledge in respect of the group and the assessed level of risk.

Component materiality applied to the subsidiary undertaking was £78,000 (2023: £79,000) based upon net liabilities (2023: gross assets). The reason for this change in basis is noted above. Performance materiality and the triviality threshold were set at £54,600 (2023: £55,300) and £3,900 (2023: £3,950), respectively, for the same reasons as for the parent company.

We also agreed to report any other differences below that threshold that we believe warranted reporting on qualitative grounds.

Our approach to the audit

In designing our audit, we determined materiality and assessed the risks of material misstatement in the financial statements. In particular we looked at areas involving significant accounting estimates and judgements by the directors and considered future events that are inherently uncertain, such as the recoverable value of the capitalised exploration expenditure within the group and the recoverable value of the parent company’s investment in the subsidiary. We also addressed the risk of management override of internal controls, including among other matters consideration of whether there was evidence of bias that represented a risk of material misstatement due to fraud.

A full scope audit was performed on the complete financial information of both components of the group by us.

Key audit matters

Key audit matters are those matters that, in our professional judgment, were of most significance in our audit of the financial statements of the current period and include the most significant assessed risks of material misstatement (whether or not due to fraud) we identified, including those which had the greatest effect on: the overall audit strategy, the allocation of resources in the audit; and directing the efforts of the engagement team. These matters were addressed in the context of our audit of the financial statements as a whole, and in forming our opinion thereon, and we do not provide a separate opinion on these matters. In addition to the matter described in the Material uncertainty related to going concern section we have determined the matters described below to be the key audit matters to be communicated in our report.

| Key Audit Matter | How our scope addressed this matter |

| Carrying value and recoverability of intangible assets (refer to Notes 3 and 12) | |

| As at 30 June 2024 and 30 June 2023 the carrying value of intangible assets totalled £4,412,453 and £3,871,362, respectively. The intangible assets relate to capitalised exploration and evaluation costs.

These capitalised costs fall within the scope of IFRS 6 Exploration for and evaluation of mineral resources and there is a risk that items have not been capitalised during the year in accordance with this Standard and with the group’s accounting policy.

The carrying value and recoverability of these assets is considered to be a key audit matter due to the level of estimation and judgement required in assessing whether or not these material assets are recoverable.

On 2 April 2024, the Group completed a Sale and Purchase Agreement (‘SPA’) to farm out of 81.25% of its 100% interest in the P2244 licence, which contains the Pilot field. Following this, during the year, a joint operating agreement (‘JOA’) was entered into by the two parties for the purposes of regulating operations under the licence and of determining respective rights and obligations of the parties.

In the current year, the P2516 license has been returned and as a result the Group recognised impairment charge amounting to £186,158 to bring the carrying value of the licences to £Nil.

|

Our work in this area included but was not limited to:

· Obtaining confirmation that the group has good title to the applicable exploration licences, including any new licences or renewals obtained during the year;

· Reviewing management’s assessment of impairment and considering whether there are any indicators of impairment as per IFRS 6;

· Reviewing the calculation of the impairment charge recorded during the year, and understanding the circumstances leading to the impairment. Ensuring this has been recorded at an appropriate amount;

· Obtaining and reviewing key terms included within the SPA relating to the farm out of the 81.25% interest in licence P2244. Obtaining and reviewing key terms included within the JOA between the two participants to the licence in order to conclude on the appropriateness of the group’s accounting policy and the accounting treatment and disclosures surrounding the transaction;

· Testing a sample of additions to ensure costs have been capitalised in accordance with IFRS 6; and

· Reviewing disclosures in the financial statements to ensure that they are in line with IFRS 6. Following the farm out agreement relating to the key licence of the Group, P2244, the group has adopted an appropriate accounting policy for the treatment of this arrangement as disclosed in Note 3.

There are a number of judgements made by management in concluding on the recoverability of the remaining intangible assets of £4,271,877 relating to licence P2244 as at 30 June 2024. These judgements are disclosed in Note 3.

Should the operator under the JOA not continue to fund development activities in accordance with the terms of the agreement, this could result in an impairment to these assets.

|

| Carrying value of investment in the subsidiary (refer to Note 15) | |

| As at 30 June 2024 and 30 June 2023 the carrying value of investment in the subsidiary totalled £5,968,544 and £5,404,044, respectively, within the parent company Statement of Financial Position. The investment in the subsidiary relates to the initial cost of investment and subsequent amounts advanced to the subsidiary that have been capitalised.

The carrying value of the investment is considered to be a key audit matter due to the material nature of the balance and the level of management estimation and judgement required in assessing whether the investment is impaired. |

Our work in this area included:

· Verifying ownership of investment held;

· Obtaining a list of additions in the year. Vouching all additions to bank and considering whether these advances are appropriate for capitalisation;

· Obtaining and reviewing the impairment assessment prepared by management and challenging all key assumptions included therein; and

· Considering whether there is evidence of impairment in accordance with IAS 36 Impairment of Assets, through reference to internal and external indicators. Considering the results of procedures performed in respect of the carrying value of exploration and evaluation assets as detailed above, given that these are the underlying assets from which the company hopes to recover the value of its investment.

|

Other information

The other information comprises the information included in the annual report, other than the financial statements and our auditor’s report thereon. The directors are responsible for the other information contained within the annual report. Our opinion on the financial statements does not cover the other information and, except to the extent otherwise explicitly stated in our report, we do not express any form of assurance conclusion thereon. Our responsibility is to read the other information and, in doing so, consider whether the other information is materially inconsistent with the financial statements or our knowledge obtained in the course of the audit, or otherwise appears to be materially misstated. If we identify such material inconsistencies or apparent material misstatements, we are required to determine whether this gives rise to a material misstatement in the financial statements themselves. If, based on the work we have performed, we conclude that there is a material misstatement of this other information, we are required to report that fact.

We have nothing to report in this regard.

Opinions on other matters prescribed by the Companies Act 2006

In our opinion, based on the work undertaken in the course of the audit:

- the information given in the strategic report and the directors’ report for the financial year for which the financial statements are prepared is consistent with the financial statements; and

- the strategic report and the directors’ report have been prepared in accordance with applicable legal requirements.

Matters on which we are required to report by exception

In the light of the knowledge and understanding of the company and its environment obtained in the course of the audit, we have not identified material misstatements in the strategic report or the directors’ report.

We have nothing to report in respect of the following matters in relation to which the Companies Act 2006 requires us to report to you if, in our opinion:

- adequate accounting records have not been kept, or returns adequate for our audit have not been received from branches not visited by us; or

- the financial statements are not in agreement with the accounting records and returns; or

- certain disclosures of directors’ remuneration specified by law are not made; or

- we have not received all the information and explanations we require for our audit.

Responsibilities of directors

As explained more fully in the Statement of Directors’ Responsibilities, the directors are responsible for the preparation of the financial statements and for being satisfied that they give a true and fair view, and for such internal control as the directors determine is necessary to enable the preparation of financial statements that are free from material misstatement, whether due to fraud or error.

In preparing the financial statements, the directors are responsible for assessing the company’s ability to continue as a going concern, disclosing, as applicable, matters related to going concern and using the going concern basis of accounting unless the directors either intend to liquidate the company or to cease operations, or have no realistic alternative but to do so.

Auditor’s responsibilities for the audit of the financial statements

Our objectives are to obtain reasonable assurance about whether the financial statements as a whole are free from material misstatement, whether due to fraud or error, and to issue an auditor’s report that includes our opinion. Reasonable assurance is a high level of assurance but is not a guarantee that an audit conducted in accordance with ISAs (UK) will always detect a material misstatement when it exists. Misstatements can arise from fraud or error and are considered material if, individually or in the aggregate, they could reasonably be expected to influence the economic decisions of users taken on the basis of these financial statements.

Irregularities, including fraud, are instances of non-compliance with laws and regulations. We design procedures in line with our responsibilities, outlined above, to detect material misstatements in respect of irregularities, including fraud. The extent to which our procedures are capable of detecting irregularities, including fraud is detailed below:

- We obtained an understanding of the company and the sector in which it operates to identify laws and regulations that could reasonably be expected to have a direct effect on the financial statements. We obtained our understanding in this regard through discussions with management, industry research, application of cumulative audit knowledge and experience of the sector.

- We determined the principal laws and regulations relevant to the company in this regard to be those arising from UK Company Law, local environmental laws, rules applicable to issuers of the AIM Market and UK-adopted international accounting standards.

- We designed our audit procedures to ensure the audit team considered whether there were any indications of non-compliance by the company with those laws and regulations. These procedures included, but were not limited to:

- Discussion with management regarding compliance with laws and regulations by the parent company and its subsidiary;

- Reviewing board minutes;

- A review of legal expenses incurred in the year; and

- Review of regulatory news announcements during the year.

- We also identified the risks of material misstatement of the financial statements due to fraud. We considered, in addition to the non-rebuttable presumption of a risk of fraud arising from management override of controls, that that the recoverable value of the capitalised exploration expenditure and the investment in subsidiaries were areas susceptible to fraud and we addressed this by challenging the assumptions and judgements made by management when auditing these significant accounting estimates as disclosed in the Key Audit Matters section above.

- As in all of our audits, we addressed the risk of fraud arising from management override of controls by performing audit procedures which included, but were not limited to: the testing of journals; reviewing accounting estimates for evidence of bias; and evaluating the business rationale of any significant transactions that are unusual or outside the normal course of business.

Because of the inherent limitations of an audit, there is a risk that we will not detect all irregularities, including those leading to a material misstatement in the financial statements or non-compliance with regulation. This risk increases the more that compliance with a law or regulation is removed from the events and transactions reflected in the financial statements, as we will be less likely to become aware of instances of non-compliance. The risk is also greater regarding irregularities occurring due to fraud rather than error, as fraud involves intentional concealment, forgery, collusion, omission or misrepresentation.

A further description of our responsibilities for the audit of the financial statements is located on the Financial Reporting Council’s website at: www.frc.org.uk/auditorsresponsibilities. This description forms part of our auditor’s report.

Use of our report

This report is made solely to the company’s members, as a body, in accordance with Chapter 3 of Part 16 of the Companies Act 2006. Our audit work has been undertaken so that we might state to the company’s members those matters we are required to state to them in an auditor’s report and for no other purpose. To the fullest extent permitted by law, we do not accept or assume responsibility to anyone, other than the company and the company’s members as a body, for our audit work, for this report, or for the opinions we have formed.

Imogen Massey (Senior Statutory Auditor) 15 Westferry Circus

For and on behalf of PKF Littlejohn LLP Canary Wharf

Statutory Auditor London E14 4HD

13 December 2024

CONSOLIDATED STATEMENT OF COMPREHENSIVE LOSS

FOR THE YEAR ENDED 30 JUNE 2024

| 2024

|

2023

|

||

| Note | £ | £ | |

| Revenue | – | – | |

| Administrative expenses | 4 | (610,940) | (671,327) |

| Pre-acquisition licence expenses | (40,071) | (129,867) | |

| Impairment of intangible assets | 12 | (186,158) | (356,532) |

| Operating Loss | (837,169) | (1,157,726) | |

| Net finance costs | 8 | (101,302) | (77,228) |

| Other income | 6 | – | 50,000 |

| Loss before tax | (938,471) | (1,184,954) | |

| Taxation | 9 | – | – |

| Loss for the year | (938,471) | (1,184,954) | |

| Other comprehensive income: | |||

| Items that will or may be reclassified to profit or loss: | |||

| Other comprehensive income | – | – | |

| Total comprehensive income | (938,471) | (1,184,954) | |

| Earnings per share (basic and diluted) – pence | 10 |

(1.26) |

(1.72) |

All operations are continuing.

The notes on pages 50 to 72 form part of these financial statements.

CONSOLIDATED STATEMENT OF FINANCIAL POSITION

AS AT 30 JUNE 2024

| 2024 | 2023 | ||

| Note | £ | £ | |

| Non-current assets | |||

| Property, plant and equipment | 11 | 1,718 | 2,508 |

| Intangible assets | 12 | 4,412,453 | 3,871,362 |

| 4,414,171 | 3,873,870 | ||

| Current assets | |||

| Trade and other receivables | 13 | 19,230 | 48,828 |

| Cash and cash equivalents | 14 | 214,977 | 109,705 |

| 234,207 | 158,533 | ||

| Total assets | 4,648,378 | 4,032,403 | |

| Non-current liabilities | |||

| Borrowings | 16 | – | – |

| – | – | ||

| Current liabilities | |||

| Trade and other payables | 17 | (1,247,235) | (567,629) |

| Borrowings | 16 | (1,095,679) | (991,339) |

| (2,342,914) | (1,558,968) | ||

| Total liabilities | (2,342,914) | (1,558,968) | |

| Net assets | 2,305,464 | 2,473,435 | |

|

Equity Ordinary share capital |

18 | 79,000 | 72,512 |

| Share premium reserve | 18 | 6,080,544 | 5,316,532 |

| Share warrants reserve | 18 | 15,000 | 15,000 |

| Other reserve | 18 | (38,848) | (38,848) |

| Retained earnings | (3,830,232) | (2,891,761) | |

| Total equity | 2,305,464 | 2,473,435 |

The consolidated Financial Statements of Orcadian Energy PLC were approved by the Board of Directors and authorised for issue on 13 December 2024.

Signed on behalf of the Board of Directors by:

Alan Hume

Director

The notes on pages 50 to 72 form part of these financial statements.

COMPANY STATEMENT OF FINANCIAL POSITION

AS AT 30 JUNE 2024

| 2024 | 2023 | ||

| Note | £ | £ | |

| Non-current assets | |||

| Investment in subsidiary | 15 | 5,968,544 | 5,404,044 |

| 5,968,544 | 5,404,044 | ||

| Current assets | |||

| Trade and other receivables | 13 | – | – |

| Cash and cash equivalents | 14 | 212,597 | 2,779 |

| – | – | ||

| Total assets | 6,181,141 | 5,406,823 | |

| Non-current liabilities | |||

| Borrowings | 16 | – | – |

| – | – | ||

| Current liabilities | |||

| Trade and other payables | 17 | – | – |

| – | – | ||

| Total liabilities | – | – | |

| Net assets | 6,181,141 | 5,406,823 | |

|

Equity Ordinary share capital |

18 | 79,000 | 72,512 |

| Share premium reserve | 18 | 6,080,544 | 5,316,532 |

| Share warrants reserve | 18 | 15,000 | 15,000 |

| Retained earnings | 6,597 | 2,779 | |

| Total equity | 6,181,141 | 5,406,823 |

Orcadian Energy PLC, company number 13298968, has used the exemption granted under s408 of the Companies Act 2006 that allows for the non-disclosure of the Income Statement of the parent company. The after-tax profit attributable to Orcadian Energy PLC for the year to 30 June 2024 was £3,818 which is attributable to bank interest income (2023: £2,779), as all costs within the group are borne by the subsidiary.

The Financial Statements were approved by the Board of Directors and authorised for issue on 13 December 2024.

Signed on behalf of the Board of Directors by:

Alan Hume

Director

The notes on pages 50 to 72 form part of these financial statements.

CONSOLIDATED STATEMENT OF CHANGES IN EQUITY

FOR THE YEAR ENDED 30 JUNE 2024

| Ordinary Share capital | Share premium

reserve |

Share warrants reserve |

Shares to be issued |

Other reserve | Retained earnings | Total | ||

| Note | £ | £ | £ | £ | £ | £ | £ | |

| Balance as at 1 July 2022 | 63,755 | 3,890,089 | 15,000 | 901,200 | (38,848) | (1,706,807) | 3,124,389 | |

| Loss for the year and total comprehensive income | – | – |

– |

– |

– |

(1,184,954) | (1,184,954) | |

| Issue of shares | 18 | 8,757 | 1,581,243 | – | (1,000,000) | – | – | 590,000 |

| Share issue costs | 18 | – | (154,800) | – | 98,800 | – | – | (56,000) |

| Total transactions with owners | 8,757 | 1,426,443 | (901,200) | – | – | 534,000 | ||

| Balance as at 30 June 2023 | 72,512 | 5,316,532 | 15,000 | – | (38,848) | (2,891,761) | 2,473,435 | |

| Loss for the year and total comprehensive income | – | – |

– |

– |

– |

(938,471) | (938,471) | |

| Issue of shares | 18 | 6,488 | 843,512 | – | – | – | – | 850,000 |

| Share issue costs | 18 | – | (79,500) | – | – | – | – | (79,500) |

| – | – | – | – | – | ||||

| Total transactions with owners | 6,488 | 764,012 | – | – | – | 770,500 | ||

| Balance as at 30 June 2024 | 79,000 | 6,080,544 | 15,000 | – | (38,848) | (3,830,232) | 2,305,464 |

Refer to note 18 for a description of the nature and purpose of each reserve within equity.

The notes on pages 50 to 72 form part of these financial statements.

COMPANY STATEMENT OF CHANGES IN EQUITY

FOR THE YEAR ENDED 30 JUNE 2024

| Ordinary Share capital | Share premium

reserve |

Share warrants reserve |

Shares to be issued |

Retained earnings | Total | ||

| Note | £ | £ | £ | £ | £ | £ | |

| Balance as at 1 July 2022 | 63,755 | 3,890,089 | 15,000 | 901,200 | – | 4,870,044 | |

| Profit for the year and total comprehensive income | – | – |

– |

– |

2,779 | 2,779 | |

| Issue of shares | 18 | 8,757 | 1,581,243 | – | (1,000,000) | – | 590,000 |

| Share issue costs | 18 | – | (154,800) | – | 98,800 | – | (56,000) |

| Total transactions with owners | – | 1,426,443 | – | (901,200) | – | 534,000 | |

| Balance as at 30 June 2023 | 72,512 | 5,316,532 | 15,000 | – | 2,779 | 5,406,823 | |

| Profit for the year and total comprehensive income | – | – |

– |

– |

3,818 | 3,818 | |

| Issue of shares | 18 | 6,488 | 843,512 | – | – | – | 850,000 |

| Share issue costs | 18 | – | (79,500) | – | – | – | (79,500) |

| – | – | – | – | ||||

| Total transactions with owners | 6,488 | 764,012 | – | – | 770,500 | ||

| Balance as at 30 June 2024 | 79,000 | 6,080,544 | 15,000 | – | 6,597 | 6,181,141 |

Refer to note 18 for a description of the nature and purpose of each reserve within equity.

The notes on pages 50 to 72 form part of these financial statements.

CONSOLIDATED STATEMENT OF CASH FLOWS

FOR THE YEAR ENDED 30 JUNE 2024

| 2024

|

2023

|

||

| Note | £ | £ | |

| Cash flows from operating activities | |||

| Loss before tax for the year | (938,471) | (1,184,954) | |

| Adjustments for: | |||

| Depreciation | 11 | 1,754 | 1,822 |

| Unrealised foreign exchange (gain) | (780) | (44,852) | |

| Impairment of intangible assets | 12 | 186,158 | 356,532 |

| Interest received | 8 | (3,818) | (2,779) |

| Finance costs in the year | 8 | 105,120 | 80,007 |

| Decrease in trade and other receivables | 13 | 29,598 | 7,001 |

| Increase in trade and other payables | 17 | 130,652 | 189,064 |

| Cash used in from operations | (489,787) | (598,159) | |

| Income taxes received | – | – | |

| Net cash flows from operating activities | (489,787) | (598,159) | |

| Investing activities | |||

| Interest received

Farm-out proceeds |

8

12 |

3,818

332,349 |

2,779

– |

| Purchases of property, plant and equipment | 11 | (964) | (916) |

| Purchases of exploration and evaluation assets | 12 | (510,644) | (1,000,638) |

| Net cash used in investing activities | (175,441) | (998,775) | |

| Financing activities | |||

| Proceeds from issue of ordinary share capital | 18 | 850,000 | 1,590,000 |

| Share issue costs paid | 18 | (79,500) | (154,800) |

| Net cash provided by financing activities | 770,500 | 1,435,200 | |

| Net increase / (decrease) in cash and cash equivalents | 105,272 | (161,734) | |

| Cash and cash equivalents at beginning of period | 14 | 109,705 | 271,439 |

| Cash and cash equivalents and end of period | 14 | 214,977 | 109,705 |

There were no significant non-cash transactions in the year to 30 June 2024.

The notes on pages 50 to 72 form part of these financial statements.

COMPANY STATEMENT OF CASH FLOWS

FOR THE YEAR ENDED 30 JUNE 2024

| 2024

|

2023

|

||

| Note | £ | £ | |

| Cash flows from operating activities | |||

| Profit for the year | 3,818 | 2,779 | |

| Adjustments for: | |||

| Depreciation | 11 | – | – |

| Interest income | (3,818) | (2,779) | |

| Decrease in trade and other receivables | 13 | – | – |

| Increase in trade and other payables | 17 | – | – |

| Cash generated from operations | – | – | |

| Income taxes paid | – | – | |

| Net cash flows from operating activities | – | – | |

| Investing activities | |||

| Interest received | 3,818 | 2,779 | |

| Funds advanced to subsidiary | 15 | (564,500) | (1,435,200) |

| Purchases of exploration and evaluation assets | 12 | – | – |

| Net cash used in investing activities | (560,682) | (1,432,421) | |

| Financing activities | |||

| Proceeds from issue of ordinary share capital | 18 | 850,000 | 1,590,000 |

| Share issue costs paid | 18 | (79,500) | (154,800) |

| Net cash provided by financing activities | 770,500 | 1,435,200 | |

| Net increase in cash and cash equivalents | 209,818 | 2,779 | |

| Cash and cash equivalents at beginning of period | 14 | 2,779 | – |

| Cash and cash equivalents and end of period | 14 | 212,597 | 2,779 |

There were no significant non-cash transactions in the year to 30 June 2024.

The notes on pages 50 to 72 form part of these financial statements.